Pian Chen and Rui Huang | April 22, 2026

Contract prices for NAND flash memory have risen sharply in the second half of 2025 as enterprise storage demand has accelerated alongside AI infrastructure investment. Prices are expected to double in 2026.[1] Despite rising demand and prices, Samsung and SK Hynix are planning production reductions in 2026 by 4.5% and 10.5%, respectively.[2] This raises key questions: Does Samsung and SK Hynix’s announced supply reductions in 2026 raise antitrust concerns?

In this study, we will evaluate how supply dynamics in the NAND flash memory market evolved from 2025 to 2026 based on public information. This article is not intended to provide any legal advice but analyzes observed supply dynamics from an economic perspective.

The NAND Market

The global NAND flash memory market is consistently valued in the tens of billions of dollars (USD 55.7 billion in 2025 and estimated USD 58.7 billion in 2026) and is projected to grow to USD 76 billion by 2031.[3]

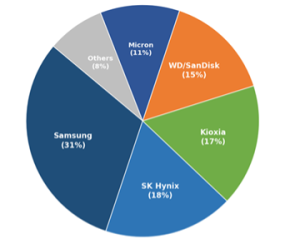

The NAND market is an oligopoly with a small number of firms accounting for the vast majority of global output. In 2025, the top two manufacturers were Samsung and SK Hynix, which account for approximately half of the global NAND market, followed by Kioxia, SanDisk, and Micron.[4]

NAND Flash Market Share (2025). Data source: UniBetter.

Entering the NAND market is challenging due to high capital and technology demands, as well as geopolitical factors. For example, Yangtze Memory Technologies (YMTC) represents China’s push to build a self-reliant semiconductor industry and reduce dependence on foreign suppliers. However, it has struggled to expand its production capacity, and its market share fell below 5% in the second quarter of 2025 due to export restrictions on advanced tools made by American companies.[5]

The Historical Semiconductor Cycles

Understanding the 2025-2026 supply restrictions requires context from the prior industry cycle. Semiconductor manufacturing has a well-known structural feature: NAND fab construction typically involves a 2- to 3-year lag between investment decisions and meaningful output, which routinely produces boom-bust cycles.

The surge in consumer electronics demand during 2020-2021 triggered aggressive capacity expansion across the industry. By the time that new capacity came online in 2022-2023, demand had softened sharply. PC shipments contracted by roughly 16% in 2022, the steepest annual decline on record. At the same time, smartphone volumes also fell globally. The mismatch between supply and demand resulted in severe downward price pressure.

Compounding the demand decline, the transition from 128-layer to 176-layer and 232-layer 3D NAND nodes increased bits-per-wafer, effectively expanding bit supply even on flat wafer starts. Since NAND is priced per gigabyte, this structural output growth accelerated the Average Selling Price (ASP) decline beyond what unit shipment figures alone would suggest.

Supply Restrictions in 2025

In early 2025, the NAND flash industry was facing mounting pressure due to a combination of weak demand, oversupply, and declining prices. TrendForce’s demand forecasts were adjusted downward from an annual growth rate of 30 percent to a more modest 10 percent to 15 percent for 2025. In response to lower-than-expected orders from PC and smartphone manufacturers, Samsung, SK Hynix, Kioxia, SanDisk, and Micron all announced plans to scale back their manufacturing operations.[6] Against the backdrop in 2022-2023, the supply restrictions announced in early 2025 were not anomalous. They were predictable corrections following an industry-wide capital overshoot triggered by the 2020-2021 demand cycle.

In the second half of 2025, Samsung, SK Hynix, and Kioxia reportedly reduced their NAND production by 7%, 10%, and 2.3%, respectively. Micron kept production in the low 300,000-unit range at its largest NAND base, the Fab 7 plant in Singapore.[7] But contradictory to its announced intention, SanDisk’s factories were running at full capacity in 2025 with production maxed out to replenish sharply reduced inventories, according to TrendForce News.[8] If the news is accurate, it indicates that not all NAND manufacturers limited supply in the second half of 2025. This divergence in behavior is notable from an antitrust standpoint: coordinated supply restriction would generally aim for more uniform conduct across alleged co-conspirators. A supply restriction scheme would be unlikely to recommend running factories at full capacity to rebuild inventories.

Supply restrictions often occur in response to declining demand and decreasing prices. In such conditions, firms may seek to restrict supply in order to stabilize or mitigate further price declines. If firms independently reduce supply, there are generally no antitrust concerns. However, if multiple firms engage in concerted actions to reduce supply, particularly when coordinated through agreements, antitrust concerns may arise.

Antitrust enforcement under Section 1 of the Sherman Act requires more than parallel conduct. Coordination typically involves direct or indirect communication between competitors, whether through explicit agreements or implicit signaling (e.g., public output reduction or pricing announcements to elicit reciprocal responses). Courts and regulators look for: firms disclosing and monitoring each other’s specific output reduction percentages; unexplained alignment in the precise timing of production cuts; and departures from independent profit-maximizing behavior.

With limited public information, it is unclear whether the supply restriction in 2025 was coordinated by all major manufacturers. Our research found no forward-looking public announcements through which the firms signaled intent to reduce supply. The public statements we found were retrospective acknowledgements, earnings call disclosures and investor communications describing reductions already implemented. The fact that SanDisk reportedly operated at full capacity during 2025 seems inconsistent with participation in an all-inclusive supply restriction scheme.

Diverging Behavior in 2026: Supply Restrictions by Samsung and SK Hynix while Cautious Expansion by Kioxia, SanDisk, and Micron

The market conditions in early 2026 have changed significantly compared to early 2025. The demand for NAND flash memory is now strong, and prices are surging. But Samsung and SK Hynix announced further production reductions for 2026. What are their economic incentives? Multiple industry sources indicate that Samsung and SK Hynix are shifting capacity toward more profitable DRAM and high-bandwidth memory (HBM) production for AI data centers.[9][10][11] Prioritizing AI memory over consumer flash storage makes economic sense when a dollar invested in HBM production generates more revenue than one spent on NAND. While this is a benign potential explanation for the production restriction, it is not a definitive account of why these firms reduced NAND output.

As AI-related demand appears long lasting, Kioxia, SanDisk, and Micron announced plans to expand capacity in January 2026.[12][13][14] These new announcements indicate that these manufacturers are responding to the increasing prices and catching up with the increasing demand for NAND flash memory.

Cautious supply expansion is economically rational. In the semiconductor sector, demand and pricing are subject to cyclical variations. When demand experiences a significant upswing, firms may rapidly scale up production capacity. However, should demand subsequently decline, these firms often carry excess capacity and suffer substantial financial losses. Drawing lessons from past cycles, firms are likely to adopt a more disciplined strategy, particularly when the sustainability of heightened demand remains uncertain. Such prudent supply management is regarded as rational economic practice and does not give rise to antitrust issues. Antitrust laws do not require unreasonable expansion of operations.

Prior Regulatory Scrutiny of Memory Manufacturers

While the current supply restrictions seem organic based on publicly available information, the industry has historically faced antitrust scrutiny with outcomes that cut both ways.

In 2002, the U.S. Department of Justice launched an investigation under the Sherman Act into DRAM manufacturers. Ultimately, five manufacturers (Samsung, Hynix, Micron, Infineon, and Elpida) pleaded guilty to participating in a price-fixing conspiracy during 1998-2002 period.[15] Samsung paid a $300 million fine, Hynix paid $185 million, and total penalties across the cartel exceeded $730 million; individual participants received prison sentences ranging from four to fourteen months.[16]

More recently, a 2018 class action alleged that Samsung, SK Hynix, and Micron coordinated to curtail DRAM production beginning in 2016, causing prices to rise sharply. The Ninth Circuit upheld dismissal of the case in 2022, finding that parallel capex reductions following Samsung’s announcement were more consistent with conscious parallelism, i.e. firms independently following the market leader, than with an unlawful agreement.[17]

On the NAND side, plaintiff firm Lieff Cabraser is currently investigating whether the five major NAND manufacturers used public statements to coordinate supply restrictions beginning in 2023, pointing in particular to forward-looking statements by Micron’s CEO predicting industry-wide reductions in capital investment and utilization rates, and Western Digital statements signaling production restraint alongside disclosure of planned NAND spending.[18]

This regulatory history matters for two reasons. First, it shows that these firms have prior exposure to antitrust scrutiny in the same product category, which is a factor courts consider when evaluating whether parallel conduct is accompanied by sufficient “plus factors” to support a conspiracy inference. Second, the Ninth Circuit’s 2022 ruling in the DRAM case is directly instructive here: the court found that capex cuts following a market leader’s announcement align with a “follow the leader” theory of conscious parallelism, under which firms can independently and rationally reach the same decision without any prior agreement.[19] That precedent is favorable to the manufacturers if similar claims arise from the 2025-2026 NAND cycle, though the presence of forward-looking, industry-wide utilization guidance (rather than purely reactive capex cuts) may present a more nuanced factual record.

Conclusion

Under Section 1 of the Sherman Act, liability arises only where there is a clear agreement among firms to restrict supply and fix prices. Parallel conduct alone does not suffice as it may simply indicate non-collusive, profit-maximizing behavior. The key economic question is whether supply restriction is coordinated or if each firm is acting independently.

Limited public information does not unambiguously imply a coordinated supply restriction among all major manufacturers. The fact that SanDisk reportedly operated at full capacity during 2025 seems inconsistent with participation in a supply restriction scheme. While Samsung and SK Hynix planned further NAND supply reductions for 2026, Kioxia, SanDisk, and Micron’s expansion announcements in January 2026 indicate that these firms are acting according to their self-interests.

This conclusion is based on publicly available information only and does not constitute legal advice. The analysis is necessarily limited by the scope of public information. Evidence of private communications, whether direct or indirect, among the firms regarding supply or pricing decisions, is not accessible through public records alone. If such evidence were to become available, it could materially change the conclusion reached here.

Sources

- Jeremy Laird, “New Report Claims Samsung, SK Hynix and Sandisk Are All Planning to Double The Price of NAND Memory Chips This Year,” January 27, 2026, PC Gamer.

- Fusion Market Intelligence, “NAND Supply Tightens,” January 22, 2026, Fusion Market Intelligence.

- Mordor Intelligence, “NAND Flash Memory Market Size and Share Analysis – Growth Trends and Forecast (2026-2031),” Mordor Intelligence.

- UniBetter Report, “List of Top NAND Flash Memory Manufacturers,” UniBetter.

- Anton Shilov, “China’s Premier Memory-maker YMTC Struggles amid Chokehold of US Sanctions,” September 28, 2025, Yahoo Finance.

- Skye Jacobs, “Memory Makers Cut Production as NAND Flash Prices Slide,” February 18, 2025, TechSpot.

- Hwang Min-gyu, “Major NAND Makers Cut Supply as Korea Firms Push Prices Up,” November 12, 2025, Chosun Biz.

- “SanDisk: NAND Undersupply Extends Beyond 2026 as Customers Seek 2027 Supply,” November 7, 2025, TrendForce.

- Felecia Smith, “Samsung and SK Hynix Plan NAND Production Cuts As SSD Prices Surge,” January 21, 2026, Technobezz.

- “SSD Prices May Follow RAM Pricing After Samsung and SK Hynix Reportedly Cut NAND Production,” January 21, 2026, TweakTown.

- “2026 Market Outlook – Focus on the HBM-Led Memory Supercycle,” January 5, 2026, SK hynix Newsroom.

- Thomas Coughlin, “Digital Storage and Memory Projections For 2026, Part 2,” January 2, 2026, Forbes.

- “Second-Tier No More: Kioxia and SanDisk Balance Alliance and Rivalry in AI NAND Race,” TrendForce, January 29, 2026, TrendForce.

- “Micron plans $24-billion Memory Chipmaking Plant in Singapore,” January 27, 2026, Reuters.

- “DRAM price fixing scandal,” Wikipedia.

- “How Samsung, Micron, and SK Hynix Built Dominance After the DRAM Cartel Scandal?” March 8, 2026, NoobFeed.

- “Samsung, Micron, SK Hynix Win Antitrust Appeal over DRAM Prices,” March 7, 2022, Bloomberg Law.

- “NAND Flash Memory Antitrust Investigation,” Lieff Cabraser.

- In Re Dynamic Random Access Memory (DRAM) Indirect Purchase Antitrust Litigation, No. 21-15125, March 7, 2022, Ninth Circuit.